Remote working public engagement exercise: local work hubs

Summary of responses to the Commonplace remote working survey.

In this page

Introduction

The COVID-19 pandemic changed the way people live, work and travel. As many as 42% of people [footnote 1] have worked away from conventional workplaces during lockdowns.

While it has been a difficult time for us all, these changed work patterns have also had many positive impacts, such as:

- a reduction in travel time and expense

- more flexibility and better work-life balance

- increased productivity

- less traffic at peak times

- less air and noise pollution

- positive impacts on local economies

For these reasons, the Welsh Government supports a long-term shift to more people working remotely. The term remote working is used to describe any work at or near a person’s home. We are creating a network of remote working hubs in towns and communities across Wales to trial this workplace option and assess demand and delivery options. It is hoped that the hubs will:

- allow people to work nearer to where they live

- allow individuals to work together in their local community

- provide a space for those who cannot or do not want to work from home

Remote working hubs give workers a third choice of work location in addition to the office or at home.

Background

Our aim for this exercise was to understand what the demand might be for local work hubs. We sought input from the Welsh public to inform the policy and contribute to our evidence base.

We worked with a supplier called Commonplace to assist with our engagement plans. Commonplace has developed a digital platform that enables local community engagement.

The platform allowed the public to drop a pin on an interactive map to show where they would like a local work hub to be. They were then asked a series of questions about their choice. Other members of the public were able to ‘like’ that area with a thumbs up icon. Information obtained included postcode and demographic details. The pin drops then generated a heat map of areas of interest for local working, which the public could view. This is still visible: Tell us your views on remote working

This bespoke engagement platform was launched in February 2021 and ran until the end of March. While the exercise is not active at present, we intend to go live again with further tranches of engagement, whether general or targeted, until January 2022.

Primary evidence gathered included:

- general attitude to remote working, and preferred working scenario

- what is important to people when working remotely (service requirements)

- how people travel to work

- respondents’ demographic information

Summary of results

Respondents have responded very positively to remote working and remote working hubs.

The numbers of respondents expressing a preference for returning to the office setting full time was very small.

A combination of drivers influenced people’s decisions, including reduced travel time and cost, better work life balance and environmental factors, such as reducing one’s carbon footprint.

While the exercise was successful, analysis of the locations of pin drops indicates that it didn’t effectively reach all sections of the community, so further targeted engagement is required.

This exercise was conducted during pandemic and lockdown conditions, so ongoing public sentiment will need to be monitored.

Options will need to be identified and appraised during the pilot period for future funding requirements of Remote Working Hubs to ensure they are affordable and sustainable for the future.

Key findings and recommendations

This survey was hosted on the Commonplace platform and promoted through GOV.WALES, Welsh Government social media accounts and public sector networks. Links were also shared to private and third sector organisations to cascade to their networks.

Demographics

Below is a summary of the demographics of respondents to give context to the findings. For full demographic information, please see appendix a: demographic information of respondents.

- 1,841 people responded to the exercise, and the page had 7,524 visitors.

- The survey results are reported descriptively, there has been no weighting of responses in relation to population data

- 62% of respondents were female

- 62% of respondents worked in the Public Sector, 8% in the private sector. 4% worked in the third sector, and 2% were self-employed. The rest of the respondents choose not to answer the question.

- 7% chose Welsh as their main language

- 65% worked full time and 5 days a week

- 23% of respondents were from Cardiff and the surrounding area

- 20% of respondents stated that they have a physical or mental condition expected to last longer than twelve months.

Recommendation

We will investigate the need for targeted engagement with specific demographic groups.

Attitude to remote working and preferred working scenario

The indication after this exercise is that respondents are interested in and feel positively about a remote working scenario, particularly a hybrid approach which could include any combination of working from home, working in a hub, and working in the office.

- 68% of respondents were either positive or mostly positive about the remote working hubs (28% positive and 40% mostly positive). Only 5% per cent stated they were negative, or mostly negative.

- Flexibility and choice were important to people - in terms of respondents’ preferred working scenario, 47% of people chose a hybrid working pattern, making this the most popular option. Hybrid working could include any combination of working from home, working in the office and working from a Remote Working Hub.

- Respondents were unwilling to pay to use a remote working hub facility - only 9% of people said they would be willing to pay with a further 15% saying they may be willing to pay depending on the level of service. 47% said they felt the employer should pay.

Recommendation

Commission a toolkit to help organisations to identify possible solutions where employees are unlikely to be positive about paying to work locally. Draft a template reciprocal agreement for space sharing across the public and third sectors.

Location preferences

The five most important requirements for respondents when choosing a location for a Remote working hub were as follows.

Respondents could choose from ten options:

- near home

- near nature and green space

- near shops

- near transport links

- near cycle paths

The options were:

- near home

- near nature/green space

- near shops

- near transport links

- near childcare/ schools

- near cycle path

- near caring responsibilities

- near gym/fitness

- near places of interest

- near places of worship.

These results point to the positive lifestyle changes people have adopted since working locally, as well as to the importance of the physical location of the building. It is encouraging to see that transport links are an important factor, suggesting that these respondents are interested in not using their cars.

Recommendation

to work closely with the Transport Division in Welsh Government in order to maximise opportunities to promote the Wales Transport Strategy and active travel agenda.

Facilities and services

In terms of hub facilities, people’s requirements were practical and perhaps to be anticipated. Broadband was the most important service to respondents, followed by an online booking system, hot-desks and meeting rooms. Suggestions on the free text option were more concerned with issues relating to lifestyle choices such as the hub being dog friendly and providing good coffee and shower facilities.

Perceived advantages to working in a local hub

When asked what advantages people saw to working from a hub, the following answers were the most popular and were evenly spread:

- improved work life balance

- increased flexibility

- save on travel costs

- improve carbon footprint

It is encouraging to see multiple motivations for remote working identified by the public.

Pre-pandemic commuting habits

It is hoped that retaining 30% of people home working will flatten the curve of traffic at peak times and thereby reduce congestion and pollution. The survey found that that 31% of people travelled over 15 miles to work before Covid, with another 28% travelling between 3 and 15 miles. 62 per cent of respondents travelled to work by car.

While not robust figures, this indicates the potential for remote working to contribute positively to the active travel agenda.

Detailed analysis of responses

Attitude

Attitude towards the remote working hubs was positive across all respondents. The group who felt most positively were private sector workers, with 75% stating they felt positively or mostly positive about the remote working hubs. (44% mostly positive, 31% positive).

The group with the lowest per centage of positive or mostly positive answers were people aged 55 to 64 with 62%, although this was also one of the lower population counts (13% of all respondents)

74% of people living in urban areas, cities or towns (see methodology) also felt positively towards the policy

In all groups low numbers (below 4%) said they felt negatively about the policy.

Recommendation

Whilst the survey sample was self-selecting and the numbers low for people aged 18 to 24, this data may still point towards the usefulness of further research into young people’s attitudes towards home working, which is often assumed to be negative.

Preferred work scenario

All groups favoured a hybrid working approach. Hybrid working was most popular amongst private sector workers, with 51% of respondents choosing this as their preferred option.

The least popular scenario amongst all groups was a return to a conventional office setting, with a share of between 5% and 5.5% of all groups choosing this option.

Between 19% and 23% chose a local remote working hub as their preferred option. All groups were positive about alternatives to an office setting with little difference between different groups.

Would you pay?

A majority of all groups stated that they would be reluctant to pay to use a hub. Only 9% of all respondents stated that they would be willing to pay. This, however, is the area with the largest difference between different groups of respondents with

26% of private sector workers stating they would be willing to pay, but only 5% of public sector workers being willing to pay.

A majority across all age groups expressed a reluctance to pay to use a hub, with between 7% to 11% saying they would be willing to pay.

Providing free to use local work hubs will need to be part of the offer in future, and the pilots will gather data so that we can devise workable options to implement the remote working hubs, and how these will be funded.

Service requirements

The top four service requirements, from a list of twelve options, were as follows:

- home

- nature/green space

- near shops

- transport links

This top four was the same for all age groups, with some small changes to the order of preference for the oldest and youngest respondents. The population sizes for both of these groups is very small, so will need further engagement to ensure a full range of views are explored. The older people are, the higher the percentage of those who wanted to be nearer home, the other factors being less important.

All sectors chose ‘Near home’ as the first option, with the same top four reasons for choosing the location. The percentage share for each category was similar for each sector. For those with caring responsibilities, being near childcare and home were most important - being near nature/greenspace and shops were also important to this group.

Mode of transport is something that will need to be monitored closely. If it is important for people to be near shops, this could indicate that people will use cars. However, it is encouraging to see transport links featuring as one of the top answers, and being near a cycle path was the fifth choice in most age categories.

When asked ‘what would you like to see in the hub’, the top four responses were:

- broadband

- booking system

- hot desks

- meeting rooms

Good broadband was the top choice for all ages, sectors, income groups, people who chose Welsh as their main language and those with caring commitments.

A greater number of self-employed people expressed a preference for the provision of meeting rooms and collaboration spaces.

Additional comments suggested respondents would like to see good coffee/ refreshments, hubs being dog friendly, bike parking and shower facilities in the remote working hubs.

Recommendation

Investigate a digital solution for a unified booking system.

Advantages to working in remote working hubs

Work Life balance was the top answer for all groups in this category; however, there are very small differences between the top four answers:

- work Life balance

- flexible working

- save travel costs

- improve my carbon footprint

This is perhaps an early indication that financial and environmental drivers are significant, as well as those related to personal wellbeing and convenience,

Transport and travel

It is hoped that the remote working policy will reduce car usage, and encourage people to use services locally.

There was little change across income groups with similar numbers using public transport.

Age group categories 35 to 44 and 45 to 54 are more likely to use the car. Younger and older people are more likely to walk, but those two groups had a very small sample size.

More private sector workers used the train, with 15%, compared to a median of 9%. People aged 35 to 44 were the most likely to walk.

In terms of pre-covid travel habits, there was very little difference across age groups - people aged 35 to 44 travelled the furthest, with the highest percentage of people in the category of travelling 15 miles and over.

42% of public sector workers travelled over fifteen miles, so a positive impact could be made if these people worked closer to home. 55% of third sector workers travelled over fifteen miles, and 45% of private sector workers, however these were both small sample sizes.

People with caring responsibilities had a slightly smaller percentage of people travelling over fifteen miles (47%) compared to those with no caring responsibilities (50%)

People living in an urban setting were more likely to travel over 15 miles to work before Covid, with 49%, as opposed to 34% of those in a rural setting.

Location analysis

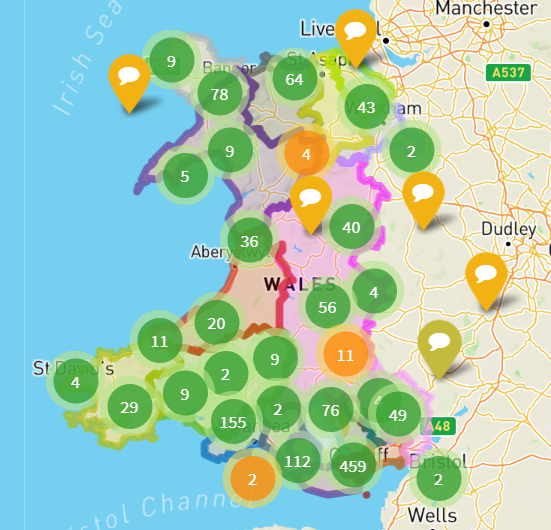

Respondents were asked to place a pin where they would most like to see a remote working hub. See appendix b: heat map of responses.

Cardiff was the area with the most pins and the area with the most respondents to the survey. There were eight pins at a single location: Chapter Arts Centre in Canton.

There were eight pins in St Mellons, suggesting interest at the edge of the city where there are fewer services.

Most of the pins were in wealthier suburbs such as Llandaff and Whitchurch, with very few in more deprived areas such as Ely and Tremorfa.

In north Wales, Menai Bridge, Anglesey and Caernarfon, an area of about forty square miles had ninety pins placed on the map, demonstrating interest - more detailed work will need to be undertaken to see how a remote working hub would benefit people living in these areas, as well as any others where respondents have shown interest.

Llandudno and the surrounding area was another popular choice, although the pins are spread out across the county of Conwy, and nine were located in the Welsh Government building in Llandudno Junction. Moving fifteen miles in-land there is a cluster of six pins in the small town of Llanwrst. Locations like this may be well suited to facilities being added to existing community facilities such as community centres or libraries.

Barry, Penarth and the surrounding area had over 100 pins placed on the map.

There are only twenty pins placed in Newport, so further engagement is required to assess interest in this area.

At a local level, it was noticeable that pin drops in areas of deprivation was significantly lower. For example, the Canton and Pontcanna areas of Cardiff had a cluster of twenty pin drops while Ely and Pentrebane had one each. Similarly central Newport had twelve pin drops, only one of which was in the Pillgwenlly area.

There are a number of possible explanations. However it sends a clear indication that more work needs to be done to engage workers and businesses in all areas with the policy.

People were asked to identify where they would like to work locally. As this does not have to be in the immediate vicinity of their home, some respondents may have decided upon an established venue outside of their neighbourhood, but still nearby. Other factors affecting this data include possible lack of suitable spaces in an area, the public reach of the exercise, the local workforce make up and lack of engagement with government in certain geographical areas.

Data gaps and weaknesses

This was a first engagement exercise to gather primary evidence about the remote working policy. Key stakeholders were contacted using traditional online methods such email, social media, Business Wales and Welsh Government websites. It should be borne in mind that this exercise was conducted under pandemic and lock down conditions, therefore some channels for signposting people to the survey were less available. The respondents were also self-selecting and could have been biased in favour of working remotely.

Our first public survey received an encouraging amount of engagement (over 2,500 comments received during its 6 week period) though it is recognised that further, targeted engagement will be needed. It was noticeable that we received limited responses in some locations of Wales – notably more deprived areas. It makes sense therefore that we focus engagement to ensure any messages, support materials and campaigns reach all workers and businesses. This will include those with protected characteristics, and current and potential Welsh Speakers.

Reaching people who have not traditionally worked remotely is important in considering the future of this way of working. It is proposed that use of different media and techniques, and perhaps outsourcing parts of the engagement programme will help achieve this.

This may include campaign material that is appropriate for different groups, such as YouTube, Blogs as well as seeking the insight of well-placed members of different communities. Citizen panels, street stalls engagement, questionnaires and other outreach activities will also help gather a response more reflective of our communities.

Options for action and future engagement

- undertake a gap analysis to establish where further engagement by demographic groups is required.

- establish modes for next phase of engagement.

- continue to run and evaluate pilots.

- establish and appraise options for funding any proposed developments.

- work with colleagues on a digital solution to the booking system.

- conduct research into the attitudes of young people to remote working.

- work closely with colleagues in the transport department to maximise opportunities to implement the Wales Transport Strategy and Active Travel agenda.

- investigate the need for targeted engagement with specific demographic groups.

Appendix a: demographic information of respondents

Where is your usual place to work (by local authority)?

| Local authority | Percentage of respondents |

|---|---|

| Didn't respond | 22% |

| Bridgend | 2% |

| Caerphilly | 1% |

| Carmarthenshire | 7% |

| Ceredigion | 3% |

| Cardiff | 29% |

| Conwy | 2% |

| Denbighshire | 2% |

| Flintshire | 1% |

| Gwynedd | 6% |

| Isle of Anglesey | 1% |

| Merthyr Tydfil | 2% |

| Monmouthshire | 1% |

| Neath Port Talbot | 2% |

| Newport | 2% |

| Pembrokeshire | 2% |

| Powys | 9% |

| Rhondda Cynon Taf | 4% |

| Swansea | 2% |

| Torfaen | 1% |

| Vale of Glamorgan | 3% |

| Wrexham | 0% |

| Outside of Wales | 2% |

Age group (% of respondents)

| Age group | Percentage of respondents |

|---|---|

| Didn't respond | 22% |

| 18 to 24 | 2% |

| 25 to 34 | 13% |

| 35 to 44 | 22% |

| 45 to 54 | 26% |

| 55 to 64 | 13% |

| 65+ | 1% |

Household income

| Household income | Percentage of respondents |

|---|---|

| Didn't respond | 24% |

| £14,999 or under | 1% |

| £15,000 to £19,999 | 1% |

| £20,000 to £29,999 | 8% |

| £30,000 to £39,999 | 11% |

| £40,000 to £49,999 | 10% |

| £50,000 to £59,999 | 10% |

| £60,000 to £69,999 | 8% |

| £70,000 to £79,999 | 6% |

| £80,000 to £89,999 | 4% |

| £90,000 and over | 6% |

| Prefer not to say | 11% |

Main language

| Main language | Percentage of respondents |

|---|---|

| Didn't respond | 22% |

| English | 69% |

| Welsh | 7% |

| Other | 1% |

Gender of respondents

| Gender | Percentage of respondents |

|---|---|

| Male | 62% |

| Female | 37% |

| Prefer not to say | 1% |

Sexual orientation

| Sexual orientation | Percentage of respondents |

|---|---|

| Straight/heterosexual | 93% |

| Bisexual | 2% |

| Gay or lesbian | 2% |

| LGBT | 2% |

| Asexual | 0.4% |

| Pansexual | 0.4% |

| Prefer not to say | 0.2% |

Do you have a physical or mental condition that is expected to last more than 12 months

| Do you have a physical or mental condition that is expected to last more than 12 months | Percentage of respondents |

|---|---|

| Yes | 80% |

| No | 20% |

Ethnicity

|

Ethnicity |

Total respondents |

|---|---|

|

White, English / Scottish / Northern Irish / British / Welsh |

1031 |

|

White, Irish |

7 |

|

White, any other background |

35 |

|

Mixed, White and Asian |

5 |

|

Mixed, White and Black Caribbean |

3 |

|

Asian, Asian Welsh, or Asian British |

7 |

|

Black, Caribbean |

1 |

|

Any other mixed or multiple background |

1 |

|

Mixed, White and Black African |

4 |

|

White, Gypsy or Irish Traveller |

1 |

|

Any other ethnic background |

5 |

|

Prefer not to say |

1 |

Religion or belief

| Religion or belief | Total |

|---|---|

| Christian | 414 |

| No religion | 582 |

| Pagan | 3 |

| Prefer not to say | 56 |

| Other religion | 13 |

| Jewish | 3 |

| Spiritual not religious | 3 |

| Shintoist | 1 |

| Humanist | 4 |

| Hindu | 2 |

| Agnostic | 3 |

| Muslim | 3 |

| Buddhist | 4 |

| None | 4 |

Appendix b: heat map of responses

Where would you like to see a remote working hub?

Footnotes

[1] Based on research by Prof. Alan Felstead, cited in “Remote Working Policy: Welsh Government Economy, Infrastructure and Skills Committee report”, January 2021.